Less-than-truckload carrier XPO is seeing the fruits of ongoing self-help initiatives, which are now intersecting with improving demand. The company said Thursday that it won market share at “above-market” rates during the first quarter. A leaner cost structure helped drive margin outperformance in the period, pushing earnings past analysts’ expectations.

Share gains in local accounts (SMBs), more customers using premium services and several AI-led efficiency initiatives are moving the needle for the Greenwich, Connecticut-based company. XPO is “hearing more positivity” from customers around capacity needs, which could propel operating ratios below 80%.

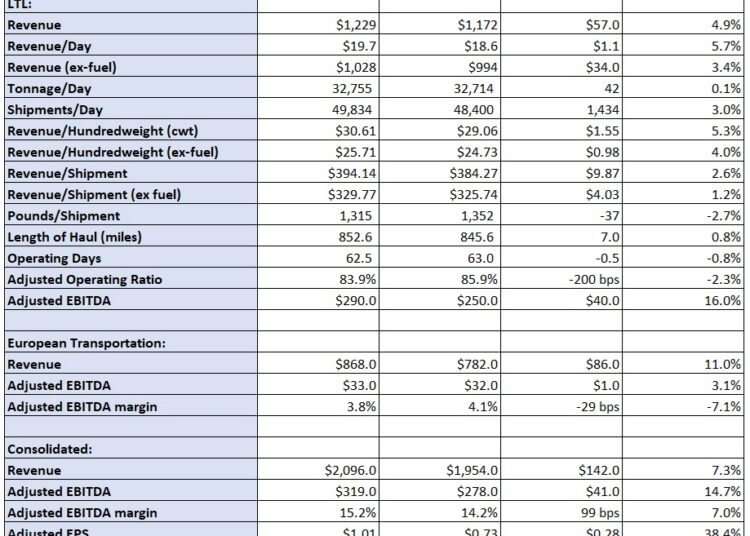

XPO (NYSE: XPO) reported first-quarter adjusted earnings per share of $1.01, which was 13 cents ahead of the consensus estimate and 28 cents higher year over year. The adjusted EPS number excluded transaction and restructuring costs. A lower tax rate was roughly a 5-cent tailwind in the period.

Consolidated revenue of $2.1 billion was 7% higher y/y and better than the $2.04 billion consensus estimate.

Table: XPO’s key performance indicators

XPO’s LTL revenue increased 5% y/y to $1.23 billion. Revenue was 6% higher on a per-day comparison. Tonnage came in flat y/y with revenue per hundredweight (yield) moving 5% higher. (Yield was up 4% y/y excluding fuel surcharges.) A 3% decline in weight per shipment and a 1% increase in length of haul were tailwinds to the yield metric.

Revenue per shipment (excluding fuel) increased 1% y/y, however, a mix shift to local accounts weighed on the calculation. These customers typically have smaller shipments sizes (lower revenue per bill), but pricing among the group is very accretive to margins. Further, management noted on a Thursday quarterly call that contract rate renewals were up by a mid- to high-single-digit percentage in the quarter.

The company is forecasting no y/y change to tonnage in the second quarter. April tonnage was down 1% y/y but tracked ahead of normal sequential patterns. Weight per shipment was up in the month and also ahead of normal seasonality.

Yield and revenue per shipment (excluding fuel) are expected to improve sequentially and y/y for the rest of the year. Management expects second-quarter yield to be “comfortably ahead” of the mid-single-digit increase seen in the first quarter. XPO’s improved service offering along with better freight selection are driving above-market pricing.

Something starting with a 7?

The LTL segment reported an 83.9% adjusted operating ratio (inverse of operating margin), which was 200 basis points better y/y and 50 bps better than the seasonally stronger fourth quarter. (The unit normally registers 50 bps of sequential margin deterioration in the first quarter.)

Revenue per shipment outpaced adjusted cost per shipment by 230 bps in the quarter. As a percentage of revenue, wages and benefits expenses declined 20 bps y/y, purchased transportation expenses moved 70 bps lower, and insurance and claims costs fell 60 bps.

Management noted a “clear line of sight” to an OR in the 70s.

It normally sees 250 to 300 bps of sequential margin improvement in the second quarter, but it expects “to comfortably outperform the high end of that range [80.9%]” this year. The outperformance would likely bring about a positive revision to its full-year margin outlook, which calls for only 100 to 150 bps of y/y improvement.

XPO’s European transportation segment reported an 11% y/y increase in revenue to $868 million. Adjusted EBITDA of $33 million was 3% higher y/y.

Shares of XPO were up 0.4% at 2:14 p.m. EDT on Thursday compared to the S&P 500, which was up 0.9%. The stock is up 57% year-to-date.

More FreightWaves articles by Todd Maiden:

Saia eyes margin turnaround amid improving demand

Old Dominion eyeing y/y margin improvement in Q2

Landstar says April yields ‘significantly’ outpacing seasonality

The post XPO could soon see sub-80% ORs appeared first on FreightWaves.