This week’s FreightWaves Supply Chain Pricing Power Index: 25 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 35 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Consumers’ critical condition collapses confidence

Despite seeing slight seasonal growth, truckload markets are showing a continued soft patch. Fears of a consumer credit crisis are becoming further justified: In the fourth quarter of 2022, 2.34% of all credit card loans were delinquent by 30 or more days. This figure is quickly approaching Q1 2020’s high of 2.76%, a level reached before consumers used their pandemic stimulus money to pay off debts.

One headwind that I might have overestimated is the impact of tax refunds this year, which I had believed would provide a short-term boost to consumer-driven freight demand. Despite the fact that 45% of Americans expect to receive a tax refund in 2023 (up from 40% last year), it is appearing more likely that such payments will have a negligible impact on truckload markets. Per data from the IRS, the average tax refund — which 43% of Americans say is “very important” to their overall financial situation — is down 11% from 2022. A majority of those receiving a return are planning to either save it or use it to pay down existing debt, not to make new purchases.

We will ultimately see how this scenario plays out, given that consumers have proven to be much more impulsive and short-sighted than analysts expect, but I am bracing for a mea culpa for the time being. This realization, coupled with weak performances in other metrics this week, has led me to drop the PPI to 25 in the interim.

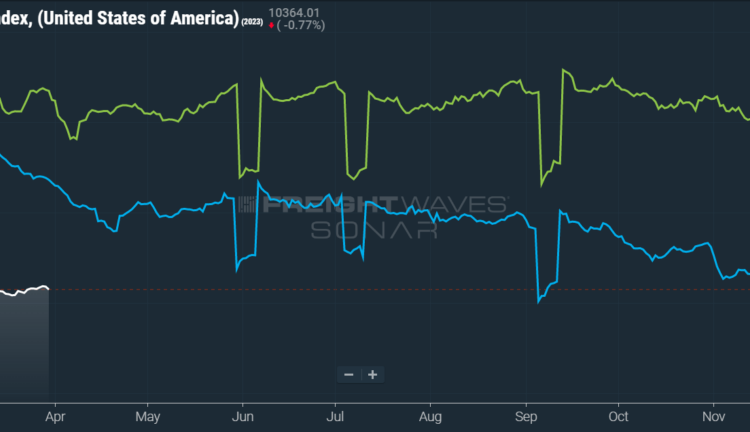

Tender volumes are well below year-ago levels:

SONAR: OTVI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ requests for capacity, ticked up a slight 0.05% on a week-over-week (w/w) basis. On a year-over-year (y/y) basis, OTVI is down 22.2%, yet such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

Accepted volumes are outpaced by 2021 and ’22:

SONAR: CLAV.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volumes (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a rise of 0.5% w/w as well as a fall of 13% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI lower.

A recent report from the World Bank underscored concerns about long-term growth in the global economy. In brief, the report’s main thesis is that a worldwide slowdown in economic growth, first set in motion by trends prior to the pandemic, is primed to endure throughout the remainder of this decade. Advanced economies, like the U.S., acutely suffer from a dwindling working-age population, declines in productivity growth (especially that of intersector productivity) and investment growth as well as a rise in government policy uncertainty. Among other consequences, this forecast weakness “curtails the resources available to pay off mounting debt loads, potentially undermining debt sustainability and leading to financial stress.”

Needless to say, this declaration — made all the more alarming given recent signals of a crisis in consumer credit — is far from optimistic. Besides the aforementioned rise in credit card delinquency rates, delinquencies are also ticking up among auto loans. Per data from Cox Automotive, loans that were delinquent by 60 or more days rose for the 10th consecutive month in February, up 21.9% y/y. These severely delinquent loans accounted for 1.9% of all auto loans in February, the highest such rate since 2006.

While consumer confidence improved slightly in March, it remains leagues below the highs of 2021 and early 2022. The survey’s Expectation Index, which measures consumers’ near-term outlook for financial conditions, remained below 80 for the 12th month since February 2022. Any reading below 80 often indicates a recession within a year’s time. Consumers also revealed that they planned to curb their discretionary spending and use their budgets for more necessary spending categories like health care, home maintenance and auto repair.

Markets see slim pickings this week:

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 72 reported weekly increases in tender volume, although activity in the larger markets ranged from muted to dismal.

In earlier columns, I have discussed how Detroit has failed to capture an influx of carriers like Los Angeles did in 2021. There are a handful of obvious causes for this difference, like the fact that California’s Ontario market is still the second-largest freight market by outbound volume, even in its current weakened condition. But another cause is that Detroit is consistently inconsistent with tender volumes. Last week, Detroit saw a 13% w/w gain in freight demand — by far the largest increase among major markets. But this week, volumes have fallen 21.2% w/w — by far the largest decline in its weight class. Ultimately, Detroit’s volumes are a bellwether for the health of America’s industrial economy, which typically moves more slowly than these weekly updates allow. But alarms coming from the industrial sector magnify such regional failures, casting doubt on the sector’s long-term health.

By mode: All things considered, reefer volumes put in a praiseworthy performance this week, though not one deserving of a standing ovation. The Reefer Outbound Tender Volume Index (ROTVI) outpaced the overall OTVI, with ROTVI rising 1.13% w/w. While such a bump is relatively minor, it comes in the wake of late-winter storms battering California and threatening to unravel 2023’s produce season.

Dry van volumes, on the other hand, received two thumbs down this week. The Van Outbound Tender Volume Index (VOTVI) tumbled 1.66% w/w. With both the current and expected weakness in consumer demand, it is unlikely that VOTVI will see any uptick in the foreseeable future.

High diesel costs spur compliance

A major driver behind OTRI’s prolonged deterioration has been the persistently high cost of diesel fuel. Though truck stop diesel prices have fallen quite a bit since their mid-2022 peaks, they are currently 42% higher than their average throughout the whole of 2019, a premium that is alternately caused by broad inflation and the destruction of U.S. refinery capacity following the pandemic.

Contract rates typically include a fuel surcharge that makes diesel a pass-through for carriers — in fact, if carriers can access diesel at wholesale prices, they can charge shippers for retail costs and pocket the change. Of course, these fuel surcharges are extraordinarily uncommon in the spot market, where carriers instead negotiate all-in prices. This simple factor has become a significant one behind increased compliance along contracted lanes (and thus OTRI’s decline), since carriers can remain mostly insulated from volatile fuel prices.

OTRI reveals overabundance of capacity in the market:

SONAR: OTRI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 3.14%, a change of 43 basis points (bps) from the week prior. OTRI is now 1,076 bps below year-ago levels, putting it closer than ever to its pandemic-induced floor.

The National Transportation Safety Board is cracking down on exemptions to hours-of-service requirements after a fatal crash in June 2021. The crash, which killed four people and injured 11, was found by the NTSB to be caused by driver fatigue and poor oversight, both of which were the primary targets of the industry’s mandated adoption of electronic logging devices. However, drivers operating under the agricultural exemption can haul for unlimited hours within their company’s 150-mile radius. Debate surrounding the efficacy of ELDs and hours-of-service exemptions continues, but it is truly unfortunate that the most recent talking point was brought about by a tragic loss of human life.

In a move that might be argued as putting the cart before the horse (or the trailer before the tractor), the California Air Resources Board (CARB) seeks to accelerate the phaseout of diesel-powered trucks, moving the target date from 2040 to 2036. CARB has yet to obtain the requisite waiver from the Environmental Protection Agency to effect such a change, but people familiar with the Biden administration’s plans say that the waiver is likely to be approved. Advocates of the trucking industry argue that this phaseout, should it accelerate, will produce yet another restraint to the state’s freight markets, which are already rocked by uncertainties surrounding AB5.

Capacity was widely available this week:

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight this week, no regions posted blue markets, which are usually the ones to focus on.

Of the 135 markets, 42 reported higher rejection rates over the past week, though 34 of those saw increases of only 100 or fewer bps.

SONAR: VOTRI.USA (white); ROTRI.USA (green); FOTRI.USA (orange)

To learn more about FreightWaves SONAR, click here.

By mode: Flatbed rejection rates compounded last week’s decline, undoing all of March’s gains and most of February’s. The Flatbed Outbound Tender Reject Index (FOTRI) nosedived by 701 bps w/w, putting FOTRI squarely back into the single digits. Coupled with the aforementioned weakness seen in industrial markets like Detroit, it is unlikely that FOTRI will see a great resurgence in the coming quarter. That said, FOTRI did manage to perform solidly in March, even as higher interest rates and manufacturers’ pessimism urged it to do otherwise. As of right now, however, it looks like flatbed markets are finally succumbing to economic pressures.

Rejection rates also declined in reefer and dry van markets, though less was at stake in their movements. The Van Outbound Tender Reject Index (VOTRI) fell 43 bps w/w to 3.01%, putting the index nearer to April 2020’s absolute low of 2.53%. Similarly, the Reefer Outbound Tender Reject Index (ROTRI) slid 26 bps w/w to 3.71%, a level already below 2020’s floor of 3.82% but above the 3.63% reading seen earlier in the month.

Blood in the water

I have spilled a ton of (digital) ink lamenting the incredible infirmity of spot market rates, so I am running out of ways to express my disappointment. Despite my usual bearishness, I’m an idealist at heart, so I held onto hope that predictions of a carrier “bloodbath” would be overstated. But it is getting harder to deny the simple fact that a great wave of capacity — especially the newer and smaller carriers — will be forced out of the marketplace, if they haven’t already locked their doors and thrown away the key.

Impossibly, spot rates find further room to fall:

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

This week, the National Truckload Index (NTI) — which includes fuel surcharges and other accessorials — fell 4 cents per mile to $2.30. The majority of this decline was driven not by falling diesel prices but by tumbling linehaul rates. The linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — lost 3 cents per mile w/w to reach $1.64.

Contract rates, which exclude fuel surcharges and other accessorials like the NTIL, also fell 3 cents per mile w/w but remain far more stable than spot rates, given the average length of shippers’ bid cycles. Contract rates, which are reported on a two-week delay, currently sit at a national average of $2.52 per mile. Weekly rises and falls in contract rates should not be given much consideration until data comes in from mid- to late March, when the effects of Q2’s requests for proposals will be seen.

SONAR: RATES.USA

To learn more about FreightWaves SONAR, click here.

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs on a seemingly weekly basis, while contract rates slowly crept higher throughout 2021.

Despite this spread narrowing significantly over the first few weeks of the year, tightening by 20 cents per mile in January, it has continued to widen again. Since linehaul spot rates remain 86 cents below contract rates, there is still plenty of room for contract rates to decline over the coming months.

SONAR: FreightWaves TRAC rate from Los Angeles to Dallas.

To learn more about FreightWaves TRAC, click here.

The FreightWaves TRAC spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, took a brutal tumble to new record lows. Over the past week, the TRAC rate fell 12 cents per mile to $1.89, a far cry from its year-to-date high of $2.39. The daily NTI (NTID), which sits at $2.31, is handily outpacing rates from Los Angeles to Dallas.

SONAR: FreightWaves TRAC rate from Atlanta to Philadelphia.

To learn more about FreightWaves TRAC, click here.

On the East Coast, especially out of Atlanta, rates remained more stable but are also outpaced by the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia slid 2 cents per mile w/w to $2.29. Except for Q4’s holiday run, rates along this lane have been dropping stepwise since July 2022, when the TRAC rate was $3.48 per mile.

For more information on the FreightWaves Passport, please contact Michael Rudolph at mrudolph@freightwaves.com or Tony Mulvey at tmulvey@freightwaves.com.

The post Too early for an April Fools’ joke appeared first on FreightWaves.