With a classic squeeze setup for a brokerage–higher spot rates to secure freight for contract business booked at a lower number–C.H. Robinson’s (NASDAQ: CHRW) first quarter 2026 earnings showed that struggle. But overall, it still came out mostly better than a year ago and in many areas sequentially as well.

C.H. Robinson’s non-GAAP earnings per share was $1.35, compared to $1.17 a year ago. More importantly, according to SeekingAlpha, that number beat the consensus forecast by 12 cents per share. Its revenue of just over $4 billion was short of consensus by $40 million.

The first reaction from investors was positive. Per Barchart, C.H. Robinson stock was up 4.6% in post-market trading, a gain of $8.54 to $194.97. It is up more than 111% in the last year, and his a 52-week high on February 6 at $203.34.

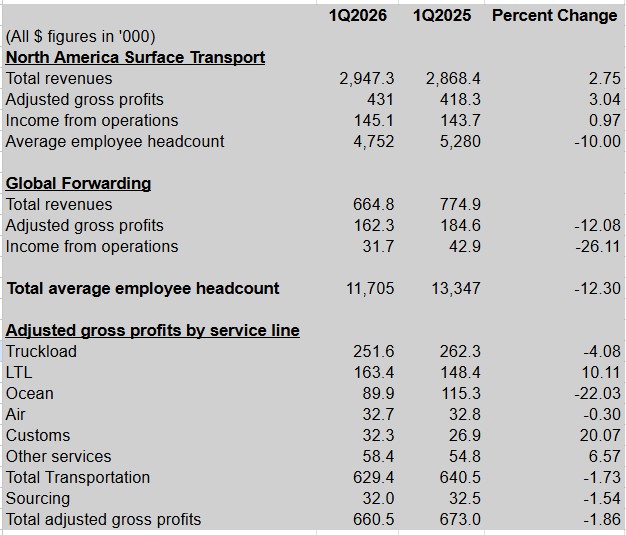

One thing that didn’t change: the 3PL continues to slash bodies. The headcount in the North American Surface Transport division, which houses its traditional brokerage activities, was down to 4,752 from 4,970 in the fourth quarter of 2025. Total headcount of 11,705 was down from 12,085 from the prior quarter.

The squeeze on the difference between revenues and the costs of transportation actually ended up mostly flat at C.H. Robinson, both down 2.1% from a year earlier.

But the net result of the tighter market given other costs was a drop in the company’s gross profit of 1.6%, to $646.6 million from $657.4 million. Adjusted gross profit declined 1.9% from a year ago.

C.H. Robinson’s operating margin was flat at 4.4% from a year earlier. The adjusted operating margin of 26.6% was up just 30 basis points. That margin excluding some restructuring costs was 29.7% compared to 27.6% a year earlier.

Sequentially, the company was mostly higher than in the fourth quarter of 2025. Revenues in the NAST group were up 4.9% from the final quarter of 2025; adjusted gross profits in NAST rose 4.7%.

The Global Forwarding business struggled sequentially, with revenues down just over 9% and gross profits down 8.8%.

Adjusted gross profits sequentially rose about 1.4% for truckload and 8.28% for LTL. Ocean was down 9.4%.

In the prepared statement released in conjunction with the earnings, CEO Dave Bozeman discussed those market conditions that are normally tough for brokers.

“As has been widely discussed in recent months, the North American trucking market has entered a period of supply-driven tightening,” he said. “As that has occurred, we’ve heard old tapes being replayed regarding which transportation providers benefit most during certain parts of the truckload cycle. But those storylines don’t fully appreciate the secular earnings growth that has consistently been generated at the new C.H. Robinson regardless of market conditions.”

More articles by John Kingston

Latest trucking nuclear verdict: $81 million, this time in Utah

Why truckers should care about DOL’s latest proposal on joint employers

TFI’s Bedard optimistic about U.S. LTL, but some of its issues persist

The post First look: C.H. Robinson mostly powers ahead in tough environment for brokers appeared first on FreightWaves.