Let’s start with something that sounds simple but changes everything about how you should read the freight market: retail is the engine that drives truckload freight.

Not manufacturing alone. Not energy. Retail.

When Americans buy things — clothes, furniture, electronics, appliances, home goods, groceries — those products move on trucks. Multiple times. From a factory to a port. From a port to a distribution center. From a DC to a regional warehouse. From a warehouse to a store or straight to a customer’s door. Every one of those moves requires a truck and a carrier. That is your business. That is the source of many loads sitting on DAT and Truckstop right now.

Here is the part that matters: when retailers change where they store product and how they move it, the load board changes with them. Different markets get busier. Different corridors tighten. Spot rates move in some regions before others. The carriers who understand that shift get positioned in the right markets. The carriers who don’t end up chasing freight that already moved somewhere else.

Right now, one of the largest shifts in retail supply chain history is underway. A survey of 250 retail supply chain executives — published by logistics providers WSI and Kase based on research from independent firm TrendCandy — documents exactly what decisions those retailers are making and where they are moving product. On its surface, this is a report written for corporate logistics teams. Read it as a spot market intelligence brief and it tells you where loads are going to concentrate over the next 12 to 24 months.

Here is how to read it.

Retail Is Leaving the Coasts and Building Out the Middle and South — More Loads in More Markets

The biggest finding in the survey: 93% of retail supply chain leaders said they plan to expand warehousing and distribution in the United States or Mexico. Eighty-five percent plan to pull at least half their supply chain footprint out of East Asia by 2028. Seventy-seven percent said they have already started shifting sourcing away from China.

For a spot market carrier, here is what that means in direct terms.

For the past two decades, most major retailers ran their supply chains through one or two massive national distribution centers. Think of the giant fulfillment campuses in Columbus, Memphis, Dallas, or the Inland Empire in California. Product came off ships in Los Angeles or Long Beach, moved inland to those mega-DCs, and then fanned out from there. The freight was concentrated. The loads were long-haul. The lanes were predictable.

That model is breaking apart. Instead of one national DC handling everything, retailers are building multiple regional distribution centers — one serving the Southeast, one serving the Midwest, one serving the Northeast, one serving Texas and the South. Smaller facilities, positioned closer to the customers they serve, pulling product from factories in Mexico and the American South instead of waiting weeks for a ship from China.

When you go from one national DC to four or five regional ones, here is what happens to loads on the board: they get shorter, they get more frequent, and they show up in markets that previously had thin freight. A 600-mile long-haul run from Los Angeles to Dallas becomes a 200-mile regional run from a Nashville DC to Atlanta retailers. A market that used to see mostly pass-through freight on I-40 now has a distribution facility generating local loads every day.

More distribution points means more loads. Shorter average hauls means more frequent loads per facility. That is a structural increase in spot market freight availability in regional markets — and it is being built right now by the executives in this survey.

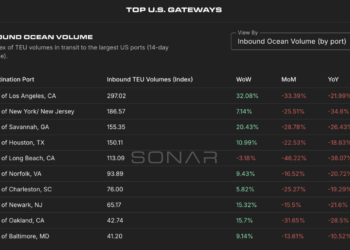

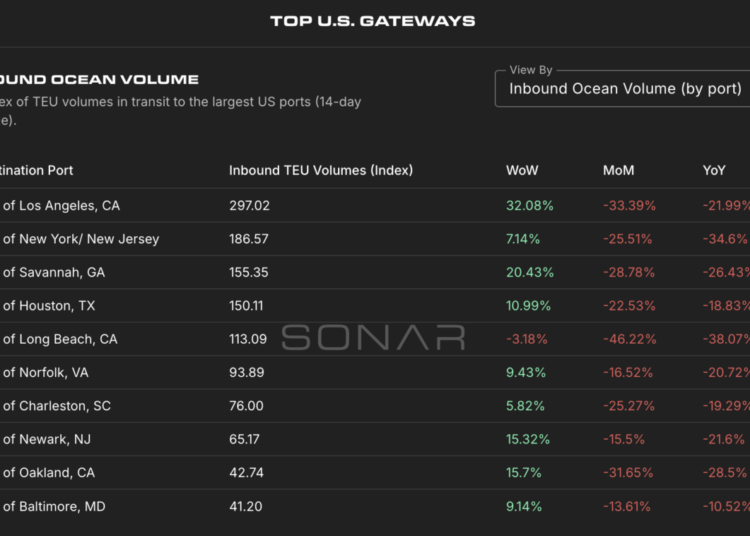

Chart: SONAR. Inbound TEU volume, gives a leading indicator into the upcoming weeks near major ports. With much of retail product usually imported to stock DCs, this can give you insight for the weeks ahead.

The Markets That Are About to Get Busier

The survey data points to specific geographic regions where freight activity is concentrating. These are not guesses — they follow directly from where the infrastructure is being built.

The South and Southeast are the primary beneficiary of retail nearshoring. As manufacturing shifts from China to Mexico, finished goods enter the U.S. through Texas border crossings — Laredo, El Paso, McAllen, Brownsville — and move into distribution networks that serve the Southeast and Midwest. The Savannah and Charleston port markets are simultaneously absorbing freight that used to run through Los Angeles as sourcing shifts to Southeast Asia and India. Both trends point to more freight in Georgia, Tennessee, the Carolinas, and the Gulf Coast corridor. If you run in any of these markets, the inbound volume feeding regional DCs is growing.

Texas is the central node of the nearshoring story. Eighty-seven percent of the surveyed executives said they have nearshoring pilots in Mexico planned within 24 months. All of that product crosses through Texas on its way north. The Laredo crossing alone handles more trade value than any other land border crossing in the country, and that volume has been climbing for three straight years. Dallas, San Antonio, Houston, and the broader Texas freight market are direct beneficiaries of that flow. More inbound means more outbound redistribution loads moving out of Texas DCs to the rest of the country.

The Midwest and Mid-South benefit from the downstream redistribution. Product that enters through Savannah or comes north from Texas eventually needs to reach stores and customers in Ohio, Indiana, Illinois, and Kentucky. Regional DCs being built in Nashville, Memphis, Louisville, and Columbus are the staging points for that redistribution. Carriers running in those markets will see growing outbound volume from those facilities as the regional networks come fully online.

The Northeast is the lagging market. The survey notes that inventory shortfalls compared to pre-pandemic levels are most acute in the Northeast and Midwest, which means when demand does recover, restocking runs in those corridors could produce significant spot market activity concentrated in a short window.

The Inventory Buffer Signal — This One Is Happening Now

Here is the most immediately actionable number in the survey: 93% of retail supply chain leaders said they are increasing buffer inventory to counter trade uncertainty.

Buffer inventory means retailers are buying and storing more product than current sales demand requires. They are hedging against tariff changes, supply disruptions, and the unpredictability of the trade environment. Every pallet of that buffer stock moves on a truck before it sits on a warehouse shelf. This is not a future trend — it is happening right now, and it is showing up as loads on the board.

When you see freight volumes in specific markets running stronger than the broader consumer demand numbers would suggest, buffer inventory building is part of the explanation. Retailers are not waiting for consumers to buy more before they order more. They are ordering ahead and storing it. That produces truck freight before the sale ever happens.

The practical implication: the spot market activity driven by inventory buffering is real, but it is temporary in any given cycle. When retailers decide they have enough buffer, the ordering pace slows and the load volume in those markets drops back (remember the huge drop off during COVID). Do not confuse inventory buffering with a demand recovery. It is a one-time freight surge that runs until the shelves are full, then stops until the next disruption triggers another round of pre-buying.

Watch for it. Run it while it is there. Do not price your business as if the rate environment it creates is the new normal.

The Load Board Is Going to Look Different in These Corridors

The survey found that the top tactical responses executives have already implemented are a roadmap for where freight is moving right now. Fifty-three percent are increasing bonded warehouse use — bonded facilities cluster near border crossings and major port corridors, so this is generating freight in those specific markets today. Forty-six percent shifted sourcing to Southeast Asia or India, which moves import volume from West Coast ports to Gulf and East Coast ports. Forty-three percent are running landed cost analysis comparing domestic versus cross-border distribution, which accelerates decisions to activate regional nodes.

All of these translate to freight in specific zip codes. The carrier running Laredo to Dallas or Houston to Memphis or Savannah to Charlotte is hauling the physical output of those executive decisions right now, whether they know it or not. Understanding the decision behind the load helps you anticipate when that freight concentration is going to shift, where the next wave of activity will appear, and how long the current market in a given corridor is likely to hold.

The Opening You Should Not Miss: 79% of Retailers Are Not Happy With Their Current Carriers

Here is the number that matters most to a carrier who picks up freight through a broker or direct shipper relationship: only 21% of retail supply chain executives said they are confident their current logistics network is equipped for the regional fulfillment strategy they are committing to.

That means 79% are not satisfied. And 84% of those same executives said they plan to restructure their 3PL and carrier partnerships to build the regional network they need. Eighty percent said they plan to do it within the next two years.

What that means in spot market terms: the freight relationships that feed loads into the brokers you already use are going through a reshuffling. New regional 3PLs are being activated to manage DC networks in markets where your truck already runs. Those 3PLs need reliable carriers in their networks before the freight starts moving. The carriers who get into those approval processes early — when the regional operation is standing up and the 3PL is actively looking for qualified trucks — are the carriers who get steady call volume from that new facility.

This is not about winning a long-term contract. It is about being a known, qualified option in your market when a new distribution operation comes online and needs trucks it can rely on. The way you do that is exactly what you are already doing: building your safety score, running on time, keeping your authority and insurance current, and being easy to work with when a dispatcher calls. The difference is calling the 3PL operating the new facility in your market before they post loads to the board, so you are already in their system when the freight starts moving.

The Technology Filter You Cannot Ignore

The survey found that the number one gap shippers identified in their current carriers was weak visibility tools — cited by 55% of supply chain leaders. In plain terms: shippers cannot see where their freight is, and they are frustrated about it.

For a spot market carrier, this matters because it affects which loads you qualify for. As regional DC networks come online and shippers tighten carrier qualification standards, basic visibility capability is becoming a requirement to get approved — not a bonus. The broker posting loads for a new regional shipper is going to ask if you have real-time tracking before they dispatch you on the first load.

Most compliant carriers already have this solved and don’t know it. If you are running a registered ELD, you have the tracking data. The question is whether you can share it with a shipper or broker in a way they can actually see. Some ELD platforms have built-in sharing links. Some TMS systems generate tracking URLs you can text to a dispatcher. If yours does, use it actively — mention it when you book loads, send the link when you are loaded, give brokers and shippers a reason to request you by name next time.

If your current setup does not have easy tracking sharing, it is worth one afternoon of research to find an ELD or load management app that does. The carriers who can answer “yes” when a new regional 3PL asks about tracking capability get into that network. The carriers who cannot get sent back to the spot board.

The Consumer Problem That Tempers All of This

Here is the honest counterweight to everything the survey says.

The loads that fill those new regional distribution centers ultimately come from consumers buying things. And right now, the consumer is under more financial pressure than at almost any point in modern history. Total credit card debt just hit $1.277 trillion — a record. The demographic that drives household formation and retail spending — people in their 20s and early 30s — is seeing its worst job market in over a decade. Diesel prices are at crisis levels because of the Iran war, which taxes both your cost structure and the consumer’s disposable income simultaneously.

What that means for you: the regional DC buildout is real. The nearshoring freight is real. The inventory buffer moves are already happening. But the full volume of freight those new distribution networks are designed to handle will not materialize until the consumer starts spending again at the pace those investments assume.

The spot market implication is direct: you will see regional markets activate as DCs come online, and you will see freight volume build in those markets over time. But you should not expect a sudden flood. The volume will build gradually as both the infrastructure and the demand mature. Run the markets that are hot now. Position yourself in the markets that are activating. But keep your break-even math honest and do not stretch your operation against a demand level that has not yet arrived.

Retail drives freight. Where retail stores product determines where loads appear on your board. Right now, retail is moving product closer to home, building new distribution points in the South and Midwest, pulling away from West Coast port concentration, and adding more inventory buffer than at any time in recent memory.

That is freight in specific markets. Some of it is on the board today. More of it will be there in 12 months. The carriers who understand the reason behind the load are the ones who see the trend before the rate reflects it — and get positioned in the right markets before everyone else figures it out.

The post When Retailers Move Their Supply Chains, Your Load Board Changes – Here Is What 250 Retail Executives Just Told You About Where Freight Is Heading appeared first on FreightWaves.