The price of ship fuel is now down to around half the post-Ukraine-invasion peak. Second-quarter fuel surcharges for containerized cargo shippers promise more savings ahead.

That’s the good news. The bad news is that if shipping ultimately switches from fuel oil to LNG or methanol as part of the energy transition, future fuel costs will likely skyrocket back to levels seen after the invasion — or higher.

The common refrain from vessel owners and operators is that cargo shippers will ultimately pay for the higher price of “green” fuel. What they probably mean is: Either cargo shippers will cover the higher price of green fuel or there won’t be an energy transition.

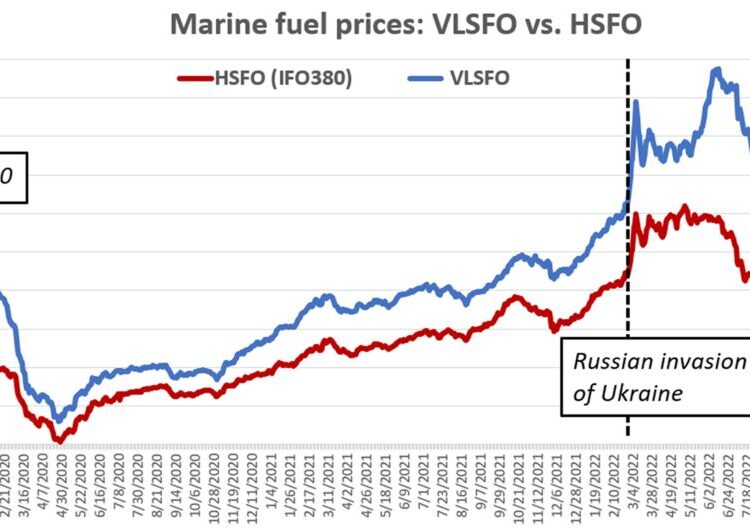

VLSFO price back to pre-war levels

Most commercial ships currently burn fuel oil with 0.5% sulfur content known as very low sulfur fuel oil (VLSFO).

Prior to implementation of the IMO 2020 regulations on Jan. 1, 2020, they burned cheaper fuel oil with 3.5% sulfur content known as high sulfur fuel oil (HSFO). Ships with exhaust-gas scrubbers continue to burn HSFO.

According to Ship & Bunker, the average price of VLSFO at the top 20 marine fuel supply hubs was $608 per ton on Thursday. That’s down 46% from the all-time high of $1,125.50 per ton reached on June 14. VLSFO pricing is back to where it was in October 2021.

Ship & Bunker put the average price for HSFO at the top 20 hubs at $476 per ton on Thursday, down 38% from the May 2022 post-invasion high and back to September 2021 levels.

Price is average for top 20 bunkering hubs. (Chart: FreightWaves based on data from Ship & Bunker)

In the container shipping sector, the trend translates into lower bunker adjustment factors (BAFs) charged to contract customers.

Distribution Publications Inc. (DPI) publishes BAF rates of carriers including CMA CGM, Cosco, Evergreen, OOCL and Zim (NYSE: ZIM). Asia-West Coast (non-reefer) BAFs for the second quarter will average $599 per forty-foot equivalent unit for these five carriers, down 13% from Q1 2023 and 32% from the peak average of $880 per FEU reached in Q3 2022.

On the Asia-East Coast route, these five carriers’ BAFs for Q2 2023 will average $1,145 per FEU, down 7% from Q1 2023 and 29% from the peak average of $1,611 per FEU reached in Q3 2022, according to DPI data.

BAFs are for dry containers, not reefers. (Charts: FreightWaves based on data from DPI)

Fuel spread is shrinking

Ships with scrubbers benefit from the discount of HSFO compared to VLSFO. Lower fuel costs increase net spot earnings and allow for higher time-charter rates.

Scrubbers are generally installed on larger ships that do long-haul runs. According to Clarksons Securities, 49% of very large crude carriers (VLCCs; tankers that carry 2 million barrels of crude) have scrubbers; 46% of dry bulk carriers in the Capesize (180,000 deadweight tons) category or larger; and 56% of container ships with capacity of 8,000 twenty-foot equivalent units or more.

The VLSFO-HSFO spread has fallen sharply over the past two months, a negative for shipowners investing in scrubbers.

The spread hit an all-time high of $420.50 per ton on July 5, 2022, according to Ship & Bunker data on average pricing at the top 20 hubs. In early February, it was still very high, at almost $240 per ton. However, as of Thursday, it was down to $132 per ton.

The spread is narrowing because VLSFO, which generally moves in tandem with Brent crude pricing, is falling faster than the price of HSFO.

Spread based on average at top 20 bunkering hubs. (Chart: FreightWaves based on data from Ship & Bunker)

In bulk commodity shipping, the spot per-day equivalent is calculated net of fuel cost (because the ship operator pays for fuel in a spot deal). Thus, the higher the VLSFO-HSFO spread, the higher the positive effect on spot income for scrubber ships, and vice versa.

Clarksons Securities calculates the dollar-per-day spot rate effect of scrubbers for various ship types. It estimates that non-eco-designed VLCCs with scrubbers earned a premium of $6,400 per day versus nonscrubber VLCCs as of Friday.

In July, the premium was almost quadruple that: $24,000 per day.

Clarksons estimates that Capesize bulkers with scrubbers earned $4,400 per day more than nonscrubber Capesizes as of Friday. In July, the premium was $18,000 per day, over four times higher.

(Charts: Clarksons Securities)

‘LNG is too expensive’

What is the outlook for ship fuel pricing? A lot depends on what happens with the energy transition. A large number of dual-fuel container ships are being built, plus a small number of dual-fuel tankers and dry bulk carriers. Virtually all of these dual-fuel vessels are designed to burn either traditional fuel oil or LNG. A small, but growing minority of dual-fuel newbuilds are designed to burn traditional fuel oil or methanol, not LNG.

Ship & Bunker tracks the price of LNG fuel versus HSFO and VLSFO at the bunkering hub in Rotterdam, the Netherlands. (It calculates the price of the volume of LNG that creates the equivalent energy as a ton of HSFO.)

As of Thursday, bunkering with LNG was 62% more expensive than with HSFO. That’s actually minimal compared to the spread in the recent past. Since October 2019, LNG bunker prices have, on average, been more than triple HSFO prices in Rotterdam, according to Ship & Bunker data.

LNG price is the price for the volume of LNG that produces the equivalent energy as 1 ton of HSFO. (Chart: FreightWaves based on data from Ship & Bunker)

The key point is this: Just because a new ship is designed to use LNG or methanol, it doesn’t mean the ship will actually burn LNG or methanol. A dual-fuel ship can just keep burning traditional fuel oil. This issue was addressed by speakers at the 17th Annual Capital Link International Shipping Forum, held on March 20 in New York.

“LNG is too expensive,” said Semiramis Palios, CEO of dry bulk owner Diana Shipping (NYSE: DSX). Palios is also president of the Hellenic Marine Environment Protection Agency and a member of Global Maritime Forum, the group spearheading the decarbonization of shipping.

“Even though dual-fuel ships do exist and are sailing at the moment, the operators are deciding to burn [fuel oil] rather than LNG because LNG is too expensive,” she said.

Knut Orbeck-Nilssen, CEO of classification society DNV Maritime, said, “If you look at the orderbook, there are nearly 900 dual-fuel vessels on order, which is quite a significant uptake over the last few years. You will have a [carbon reduction] benefit of around 25% if you do run on LNG. But that is the problem: None of these vessels currently are running on that fuel. We also have to realize that LNG is a hydrocarbon.”

Mark O’Neil, CEO of Columbia Shipmanagement, highlighted the practical hurdles to the fuel transition for shipping.

“Do we really believe that given the peripatetic and fragmented nature of the shipping sector, that a fossil-fuel-free and carbon-zero future is what is in front of us?

“I’m sorry to say that proposition doesn’t stand up to scrutiny, particularly when you also look at the geopolitical situation we currently face, where you have the relations between the U.S., China, Europe, India and Russia coming more and more to the fore. Do we really believe that this is an environment in which the green revolution can or should take place?” asked O’Neil.

Green methanol push requires government support

As expensive as LNG is compared to fuel oil, green methanol looks even more expensive. It remains unclear whether the private sector alone, without government intervention, can make pricing work.

Container shipping giant Maersk is at the forefront of the push for green methanol. It has 19 methanol-fueled newbuildings on order, with related capital expenditures totaling almost $3 billion.

During A.P. Moller – Maersk’s annual general meeting on Tuesday, Chairman Robert Maersk Uggla conceded that “ensuring the availability of the green fuel required to power these vessels is quite a challenging task.” Maersk has signed MOUs with nine green methanol producers “but even greater production and scale is needed.”

“When we started this journey, all of our competitors were ordering ships with LNG-fuel engines. LNG may be a really good fuel if you want to reduce sulfur emissions, but it leads to significant methane slip. As per our life cycle analysis, it’s actually more damaging to the environment than some other conventional hydrocarbon fuels,” argued Uggla.

“So, I’m glad to see some of our competitors actually following AP Moller – Maersk in terms of ordering not LNG ships but ships that can actually use green methanol.

“But what is very important for people to understand is that this change will not happen just because of private initiatives,” he warned.

“Green methanol still comes at a significant premium to hydrocarbons and many customers are not willing to pay for that. So, it is critical that governments provide the right incentives and also provide support for the development of green fuels so that these fuels can become competitive.”

Click for more articles by Greg Miller

Related articles:

How push to decarbonize shipping slowed tanker building to a trickle

Price of ship fuel falling even as Russia-Ukraine war rages on

The sinking price of ship fuel: Near prewar levels after summer plunge

Ships that ‘scrub’ emissions earn twice as much as those that don’t

Ship fuel enters uncharted territory as prices hit new wartime peak

Ship fuel spikes to historic $1,000/ton mark as war fallout worsens

Price of ship fuel surging, poised to eclipse all-time high

Ship fuel price highest since 2013, ‘scrubber spread’ widens

The post Ship fuel cost way down from war peak, but ‘green’ fallout looms appeared first on FreightWaves.