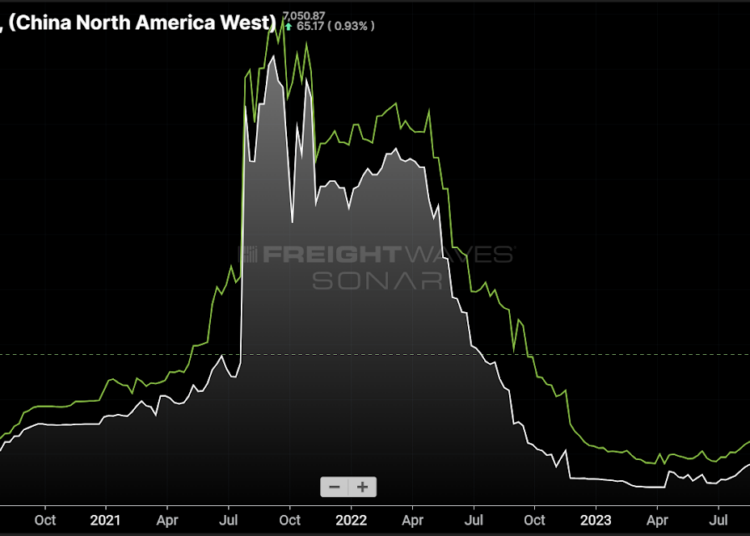

Chart of the Week: Freightos Baltic Daily Index – China to North America West and East Coast SONAR: FBXD.CNAW, FBXD.CNAE

Spot rates for shipping forty-foot equivalent containers over the ocean from China to North America hit their highest levels since the summer of 2022 and are still climbing. Supply chain disruption has returned to the maritime industry, but how does it compare to the pandemic era and is it sustainable?

Reliable sourcing drives efficiency in any company’s supply chain. If goods and their subsequent transportation are consistently available, then businesses can put less effort into forecasting and managing inventories. These were the primary concerns during the pandemic.

The pandemic-era supply chain debacle was caused by a series of factors:

Spiking demand for goods well beyond expectations.

Limited production availability due to quarantining.

Insufficient transportation capacity.

Limited port infrastructure.

Panic ordering by companies due to the above.

Issues 1, 2 and 4 are not present in the current environment, but 3 and 5 are. The increase in order lead times impacts all downstream transportation and logistics.

Demand is not really the issue

Goods demand has been relatively stable over the past few years, though it has been better than many economists expected. Orders for durable goods fell slightly year over year in May.

The Inbound Ocean TEUs Volume Index (IOTI), which measures bookings of twenty-foot equivalent containers from China to the U.S., is up 15% year over year but down 13% from 2023 peak levels hit last August when rates were roughly a quarter what they are now. Demand has been increasing steadily since May, but not at a particularly alarming rate compared to last year.

Capacity troubles

The Israel-Hamas war that began in October last year has destabilized one of the primary shipping routes in the world. Houthi rebels based in Yemen continue to attack ships in the Red Sea, forcing many carriers to extend their trip by an average of 10-12 days. This extended trip removes nearly two weeks of capacity and service from each vessel that normally travels through the Red Sea.

While this does not directly impact most of the transportation capacity on goods heading from Asia to the U.S., it does indirectly pull from the overall pool of available ships. This diversion impacts more than 25% of the global capacity, according to Flexport.

There have been claims of some level of capacity management, which is difficult to say definitively, but average vessel capacity for ships moving from China to the U.S. is down about 8% y/y in June. This downward trend has been relatively consistent since last September. Seasonality and the Red Sea diversion could explain some but probably not all of it.

Service deterioration could be more of the problem as shippers may have expected transits to stabilize sustainably after the pandemic. The average port pair delay has grown from three to five days over the past year while published transits have been relatively flat from China to the U.S.

Rejection rates have been averaging higher since last November as well, moving from about 8% through most of 2023 to above 10% most of this year. The current value of 14.5% is the highest point since the start of the Red Sea issues.

Climbing the peak

Peak season for maritime imports has traditionally been in July and August. Many wonder if the current demand growth is the result of an increase in orders being pulled forward to ensure on-time delivery and availability.

If true, then the next two months’ IOTI will be flat. If not true, then there will be more pressure on rates and capacity. The U.S. transportation market will also feel these effects as the growing imbalance of goods adds to international container shortages.

This could be a boon for domestic intermodal and some level of boost to the still overcapacity-laden trucking industry. While this does not look like the chaos of the pandemic era, it does look like supply chains will be much more challenged than they were last year.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

The post Maritime shipping still on troubled waters appeared first on FreightWaves.