Asset-light transportation provider Forward Air reeled in its 2023 full-year outlook Tuesday but said the rate at which volumes have been declining has slowed in the last couple of weeks.

Forward (NASDAQ: FWRD) reported first-quarter earnings per share of $1.37 Monday after the market closed, 7 cents better than Seeking Alpha’s consensus estimate but 20 cents lower year over year (y/y).

The result benefited by 24 cents due to the reversal of an incentive comp accrual as the freight market softened further. Interest expense was a 4 cent headwind compared to the year-ago quarter on only a slight increase in outstanding debt.

The company now expects full-year EPS in a range of $6.20 to $6.60, which assumes the “freight environment will significantly improve in the second half of the year.” The outlook is down from management’s initial take on the year provided in October, which called for y/y EPS growth (Forward Air posted adjusted EPS of $7.18 in 2022).

The new guide bracketed the consensus estimate of $6.32 at the time of the print and implies nearly 60% of Forward’s earnings will occur in the second half of the year.

Chairman, President and CEO Tom Schmitt told analysts on a Tuesday call that the company is seeing good demand from two end markets where it has a large presence. Consumer discretionary income is currently skewed toward services and events, which is a tailwind for Forward, and demand for medical technology and devices remains consistent.

On demand expectation from its customers: “Deliveries from Asia to our customers are expected to get closer to a normal size and normal frequency by the end of this quarter,” Schmitt said. “That’s not what every single one of them is saying but if you had to get a mean, or expected midpoint, that’s what we’re hearing from the vast majority of them.”

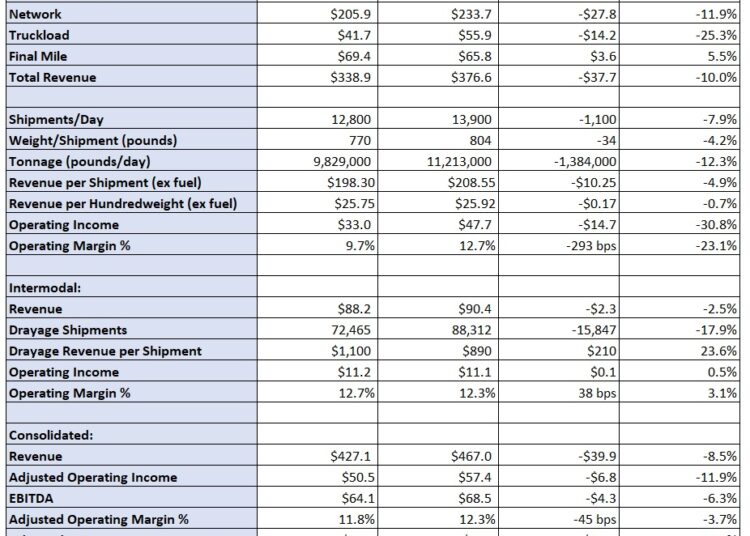

Table: Forward’s key performance indicators

Consolidated revenue of $427 million was down 9% y/y in the first quarter and worse than management’s flattish guidance (down 4% to up 2%).

Revenue in the expedited freight segment, which includes less-than-truckload, truckload and final mile, fell 10% y/y to $339 million. Tonnage per day was down 12%, the combination of an 8% decline in shipments and a 4% decline in weight per shipment. Revenue per hundredweight, or yield, was down 1% excluding fuel surcharges with revenue per shipment (excluding fuel) down 5%.

Shipments in the quarter were fewer and lighter than a year ago. The number of “pieces” in each shipment was down 16% y/y. Overall shipment weights were also lighter due to fewer pieces. Weight per piece, however, was up 12.7% y/y.

The tonnage declines have eased from the start of the year. January tonnage was down 16% y/y, February was down 9% and March was off 11%. Tonnage was down 8% in April but only 5% lower in the most recent weeks, which could be “the beginnings of an improving freight environment.”

The per-hundredweight yield calculation benefited from lower shipment weights but was dragged down by a 6.7% decline in length of haul. Schmitt contended the company is pricing its freight appropriately, pointing to revenue per ton mile excluding fuel surcharges, which was up between 2.5% and 4% y/y.

“Revenue per ton mile (ex-fuel) in my mind is pound for pound the best metric for what we get paid for, for the same effort expended. … We’re getting paid more for the same work that we did a year ago,” Schmitt said.

The expedited unit recorded 290 basis points of operating margin decline to 9.7%.

All expense lines increased as a percentage of revenue except purchased transportation, which was down 430 bps y/y. Forward has been actively reducing the number of miles third-party providers execute. Third-party linehaul miles were down to 5% of the total in the quarter compared to 25% a year ago.

Schmitt said the first quarter was likely the bottom of this freight cycle and indicated some conservatism in the company’s new full-year outlook.

“I don’t want to overestimate and then disappoint,” Schmitt said. “I do see real improvements. … I expect the odds of us beating what we put out to be better than missing it.”

Intermodal revenue dipped 3% y/y to $88 million with shipments off 18% and revenue per shipment up 24%. The operating margin improved 40 bps to 12.7%.

Forward’s second-quarter guidance calls for revenue to decline between 7% and 17% y/y, implying $453 million at the midpoint of the range, which was lower than the $481 million consensus estimate. It expects EPS of $1.28 to $1.32 versus consensus at $1.65.

Excluding the accrual benefit in the first quarter, the midpoint of the second-quarter EPS range is 15% higher sequentially.

More FreightWaves articles by Todd Maiden

Supply chain index hits all-time low in April

Saia’s stock pops 15% on lone LTL earnings beat

ArcBest defends dynamic pricing strategy

The post Forward Air dials down 2023 outlook but sees ‘real improvements’ appeared first on FreightWaves.