Russia — one of the world’s top energy providers — is mired in war. The OPEC cartel is cutting production. And yet, oil prices continue to fall, weighed by global recession fears and concerns on Chinese demand.

For ocean shipping, this translates into cheaper marine fuel costs, a positive for operating margins, and much narrower fuel spreads, a negative for owners of vessels with exhaust gas scrubbers.

For listed tanker owners, the drop in oil prices is coinciding with faltering sentiment and falling share prices at the very time vessel supply fundamentals point to a sustainable rate rebound.

Deutsche Bank shipping analyst Chris Robertson said late Tuesday, “We believe the market will more heavily discount energy exposed companies, including tanker owners, based on current downside demand risks and negative macroeconomic sentiment. Oil prices have been on the decline over the past few weeks, falling further this week on weak manufacturing data out of China.”

As a result of macro issues and “fear and uncertainty in the market,” Deutsche Bank lowered its 12-month price target for product-carrier owner Scorpio Tankers (NYSE: STNG) by 15%, to $55 per share from $65. It closed Tuesday at $48.54.

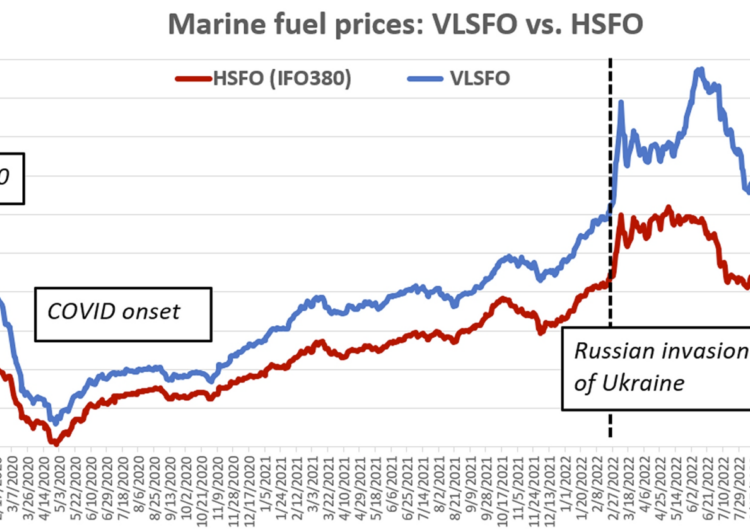

Marine fuel prices back to 2021 levels

Most commercial ships burn fuel with 0.5% sulfur known as very low sulfur fuel oil (VLSFO). The use of VLSFO or other low-sulfur fuels has been required since implementation of the IMO 2020 environmental regulations on Jan. 1, 2020.

There is an exception for ships with exhaust gas scrubbers. They can continue to burn cheaper 3.5% sulfur fuel known as high sulfur fuel oil (HSFO).

Ship & Bunker reported that the average price of VLSFO at the world’s top 20 refueling hubs had fallen to $593.50 per ton on Monday. This is roughly half the high reached in June 2022, in the wake of Russia’s invasion of Ukraine. VLSFO prices are now on par with December 2021 prices.

The price of HSFO at the world’s top 20 hubs was $496.50 per ton on Monday. That’s down 35% from the peak in May 2022 and back to levels seen in September 2021.

(Chart: FreightWaves based on data from Ship & Bunker)

VLSFO-HSFO spread below $100 per ton

The price of VLSFO has fallen steeply, in line with the drop in Brent crude, whereas the price of HSFO has held up better. This has significantly narrowed the VLSFO-HSFO spread.

Ship & Bunker data for the top 20 refueling ports shows an ignominious milestone on Monday: The spread breached the $100-per-ton threshold, closing at $97. This is less than a quarter of the all-time high reached in July 2022 and down to levels seen in October 2021.

(Chart: FreightWaves based on data from Ship & Bunker)

The decline has been precipitous. Over the past three months, the spread has fallen 60%.

In bulk commodity shipping, the per-day-equivalent spot rate is calculated net of fuel cost (because the ship operator pays for fuel in a spot voyage). Thus, the higher the VLSFO-HSFO spread, the higher the positive effect on net spot income for owners of scrubber-equipped ships, due to their fuel cost savings — and vice versa.

Clarksons Securities calculates the dollar-per-day spot-rate effect of scrubbers for various ship types. It estimated that a non-eco-design very large crude carrier (VLCC; a tanker that carries 2 million barrels of oil) with scrubbers earned a premium of $6,000 per day versus a nonscrubber VLCC as of Tuesday.

In July 2022, the premium was quadruple that: $24,000 per day.

Clarksons estimated that a bulker in the Capesize category (with capacity of around 180,000 deadweight tons or DWT) with scrubbers netted $4,200 per day more than a nonscrubber Capesize as of Tuesday. Last July, the premium was $18,000 per day, over four times higher.

(Chart: Clarksons Securities)

Prediction for $100-$250 spread range

Scorpio Tankers is one of many publicly listed shipping companies that invested heavily in scrubbers to take advantage of the VLSFO-HSFO spread.

On a conference call Tuesday, James Doyle, Scorpio’s head of corporate development, was asked whether the dwindling spread was structural.

“I don’t think it’s structural,” he replied. “If you look at demand for HSFO, it’s predominantly for vessels with scrubbers and for power generation in the Middle East. I think the pressure is from distillate [on VLSFO prices].

“You’ve seen distillate cracks come down. You’ve seen diesel prices come down. And I think it’s just a reversal of what we’ve seen over the last two years. You [previously] had a very, very strong, very tight distillate market. People had been worried about shortages. So, it is probably an overreaction to that.

“For the foreseeable future, we are still constructive on the spread. Does it hit the high $300s [per ton] as it has in the past? Maybe not, but I think $100 to $250 is a reasonable range.”

US trucking woes curb global diesel demand

Commenting on global distillate demand, Doyle referred to trucking weakness. The U.S. trucking sector is now doing so badly that it is being talked about on a product tanker conference call — likely a first.

The Department of Energy weekly diesel price used for most trucking surcharges continues to fall. The price Monday fell to $4.018 per gallon, the lowest level since February 2022.

(Chart: FreightWaves SONAR)

According to Doyle, “While we do expect slightly lower diesel demand due to less trucking activity, the increases in gasoline, jet fuel and naphtha demand more than offset the lower distillate demand. We expect refined product demand to average 1.5 to 2 million barrels per day more from Q2 to Q4 than last year and go up throughout the remainder of the year.

“For almost two years we’ve seen massive draws in inventories. Right now, we look at a market where Russia has been able to export more products than pre-sanction levels, but it’s unclear if they will be able to maintain those levels of exports in the long term.

“And we are seeing inventories continue to decline despite higher volumes. So, I think as we move into the back half of this year, [tanker] demand is going to increase from a gasoline, jet fuel and naphtha perspective and it’s going to be much more than a slight drop in distillate demand from trucking.”

Tanker stocks keep falling

Both crude-tanker stocks and product-tanker stocks have been following roughly the same trajectory as Brent crude prices over recent months.

Brent fell through the first half of March, rose through the second half of March, moved higher still after the OPEC cuts announcement in early April, peaked in mid-April, then turned downward.

Most tanker stocks fell through mid-March, rose again through mid-April (temporarily diverging from crude in the immediate wake of the OPEC announcement in early April), and have been dropping ever since.

Price change since March 1. CBN23: Brent crude; STNG: Scorpio Tankers; FRO: Frontline (NYSE: FRO); EURN: Euronav (NYSE: EURN); NAT: Nordic American Tankers (NYSE: NAT); ASC: Ardmore Tankers (NYSE: ASC); TNK: Teekay Tankers (NYSE: TNK). (Chart: Barchart)

Brent crude closed Tuesday at $75 per barrel, below where it was when OPEC announced its latest round of cuts. The bearish view is that oil prices are falling due to negative expectations on future demand. This would presumably equate to lower volumes of crude and products at sea.

Scorpio Tankers President Robert Bugbee — ever the optimist — doesn’t buy that.

“There are two red herrings we see. One red herring is ‘Oh my God, we are seeing these newbuilding orders. [Tanker orders have recently increased off historic lows.] The other is this thing to do with recession and headline demand.

“Just with the increase in jet fuel going around the world, which is a tremendously important thing for the product market, we can’t get to a scenario over these next quarters where you do not get continued product-tanker demand. And that’s without even dealing with trying to refill inventories, which is required,” said Bugbee.

Earnings roundup

Scorpio Tankers’ profits, rates and dividends are up and its debt its down. Nevertheless, like other tanker names, its stock continues to fall.

Shares of Scorpio are down 19% since March 1. The share price fell 5% Tuesday in more than double average trading volume. (Brent also fell 5% on Tuesday and the stock market overall was down.)

Scorpio reported net income of $193.2 million for the first quarter of 2023 versus a net loss of $84.4 million in Q1 2022. Adjusted earnings per share of $3.31 topped the consensus forecast for $3.15.

Quarter-to-date rates in Q2 2023 were also higher than analysts predicted.

Scorpio has 39% of its Q2 2023 available days for its LR2s (80,000-119,999 DWT capacity) booked at $53,000 per day; 35% of available days for its MRs (25,000-54,999 DWT) secured at $37,000 per day; and 34% of its available days for its Handymaxes (10,000-24,999 DWT) at $37,000 per day.

According to Evercore ISI analyst Jon Chappell, “It is dangerous to extrapolate quarter-to-date figures, especially given the volatility of the market of late … but these rate estimates underwrite a Q2 2023 cash-flow outcome that is well above current expectations.”

Click for more articles by Greg Miller

Related articles:

Tanker shipping stocks sink despite talk of looming rate boom

Ship fuel cost way down from war peak, but ‘green’ fallout looms

Price cap on Russian crude could soon face its biggest test

European tanker owners make a fortune off Russian oil trade

OPEC+ throws tanker shipping a curveball, shaking confidence

China-Russia vs. US-EU: How global shipping is slowly splitting in two

In search of shipping’s next supercycle: Are tankers next?

Tanker shipping consolidation saga watched ‘like it’s Netflix’

How push to decarbonize shipping slowed tanker building to a trickle

The post As oil tumbles, marine fuel gets cheaper — and so do tanker stocks appeared first on FreightWaves.