This week’s FreightWaves Supply Chain Pricing Power Index: 40 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 35 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 40 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

A booming ‘quiet season’

By most metrics, freight markets are showing clear signs of a lasting recovery. Since the nature of this recovery tends to stoke controversy among industry analysts, it is well worth clarifying what the term does and does not entail. The current upturn (such as it is) implies growing distance from the market’s cycle low, which occurred in May 2023. Shippers’ demand was more or less stable in the back half of last year and continues to gain strength into 2024 thus far. In short, the early stages of this recovery are characterized by a rebalancing market, a return to normalcy after a four-year roller coaster of volatility.

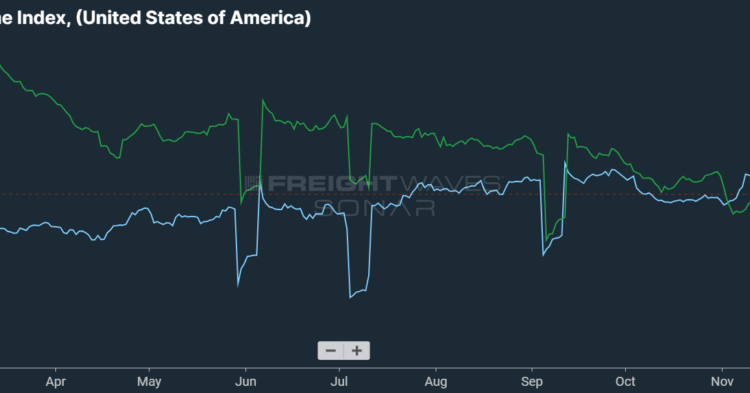

SONAR: OTVI.USA: 2024 (white), 2023 (blue) and 2022 (green)

To learn more about FreightWaves SONAR, click here.

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ requests for capacity, is down 1.72% week over week (w/w). On a year-over-year (y/y) basis, OTVI is up 5.54%, though such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be inflated by an uptick in the Outbound Tender Reject Index (OTRI).

SONAR: CLAV.USA: 2024 (white), 2023 (blue) and 2022 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volume (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a rise of 1.46% w/w as well as a fall of 3.78% y/y. This positive y/y difference implies that actual freight flow is recovering from this cycle’s bottom.

But what this recovery is not — at least, not presently — is immediate and rapid growth in freight demand that can satisfy the excess capacity lingering in the market. Some industry participants have had their expectations for growth shaped or reshaped by the historic rally seen throughout 2020-21. These expectations should be tempered, as they will almost certainly lead to disappointment otherwise.

The U.S. consumer has been remarkably resilient over the past two years, despite numerous indications that cautioned to the contrary. Whether consumers can continue to not only sustain but grow their spending on freight-intensive goods in 2024 is a risky bet to make. This risk is compounded by the potential for retaliation from the Federal Reserve, which could respond to a too-hot goods economy with further monetary tightening.

A broad economic recession, then, is the most obvious threat to recovery. In December, the total amount of consumer credit rose by a paltry $1.6 billion, 90% below consensus expectations of a $16 billion surge. Revolving credit (which includes credit card debt) was responsible for the lion’s share of this minor gain, rising by $1.1 billion in the month. This waning reliance on credit cards could be a bullish signal that consumers are interested in long-term financial health, if not for the fact that the personal saving rate also tumbled to a 12-month low of 3.7% in December — a level nearly half of its pre-pandemic average. Without excess spending or saving, it simply looks like the consumer is in a tight spot.

While the U.S. consumer has been known to pull a rabbit out of the hat before, there are other threats to this burgeoning recovery. The excess capacity that entered the industry during the gold rush of 2020-21 has — like the U.S. consumer — proved tenacious in remaining within the market. If this tenacity persists, it would delay if not disrupt a full recovery. Geopolitical powder kegs might also reignite inflation: Although the U.S. is relatively insulated from recent developments in the Red Sea, there is a nonzero possibility that discrete conflicts in the Middle East, Eastern Europe and (potentially) East Asia could coalesce and further jeopardize global trade.

By mode: Reefer demand has fallen quite a bit since late January, when it peaked off the back of severe winter storms that rocked much of the contiguous U.S. Reefers are used not only to insulate temperature-sensitive freight against sweltering heat in the summer, but also to protect goods from the winter cold. But as temps have stabilized above their 30-year average, the Reefer Outbound Tender Volume Index (ROTVI) is down 5.43% y/y. Still, ROTVI is up a slight 0.07% w/w, and it looks as though another round of cold weather is just around the corner.

Van volumes, meanwhile, have been more or less stable after recovering from mid-January’s mighty dip. The Van Outbound Tender Volume Index (VOTVI) is currently down 2.24% w/w but is up 10.21% y/y. A coming wave of imports from China should sustain truckload markets in Southern California and the surrounding region for some time, though the Lunar New Year celebrations will prove to be a headwind that takes effect in the next few weeks.

Slowly but surely

Aside from a brief and shallow dip on Wednesday, OTRI has remained above 5% since mid-January. A rising OTRI can be an inflationary force to spot rates if it tracks above (roughly) 7%, or if it makes rapid gains over a short period of time. While OTRI currently displays neither of these signals, it is a positive sign that excess capacity is indeed leaving the market.

SONAR: OTRI.USA: 2024 (white), 2023 (blue) and 2022 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, fell to 5.06%, a change of 22 basis points from the week prior. OTRI is now 158 bps above year-ago levels, another point of optimism for 2024’s recovery.

Demand for new Class 8 trucks at the end of 2023 was softer than expected, as it seems that disruptions to production caused by the semiconductor supply crisis have finally ceased to be a major source of upward pressure. According to data from ACT Research, December saw orders fall 14% y/y to 26,350 trucks. This month capped off a year in which orders totaled 278,270 — enough to meet ACT Research’s replacement rate of 275,000 but down 7% from 2022’s banner year. Prices of used trucks also continued to moderate in Q4, with a 3-year-old truck going for an average of $67,000, or nearly half of what it cost in Q2 2022.

Hot and cold

Spot rates had an impressive rally at the end of January, thanks in large part to OTRI’s surprising tightness. Since then, however, rates have come off their peak but are still in line with early December’s high. If the aforementioned threat of severe winter storms does come to fruition in the coming weeks, it is more than likely that spot rates will rise accordingly.

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

This week, the National Truckload Index (NTI) — which includes fuel surcharges and other accessorials — fell 8 cents per mile to $2.34. Sliding linehaul rates were wholly responsible for this week’s loss, as the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — fell 8 cents per mile to $1.73.

Contract rates, which are reported on a two-week delay, are stabilizing at the end of January after giving up all of their holiday gains. The quickness with which contract rates lost their holiday momentum is an early indication of the pricing power that shippers exercised in the ongoing bid cycle. For the time being, contract rates — which exclude fuel surcharges and other accessorials like the NTIL — are unchanged on a weekly basis at $2.33 per mile.

To learn more about FreightWaves SONAR, click here.

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs seemingly weekly, while contract rates slowly crept higher throughout 2021.

Over the course of 2023, this spread averaged 10 cents lower than in 2022, indicating that contract rates had yet to come into balance with the market’s fundamentals of carriers’ supply and shippers’ demand. These lopsided fundamentals were more appropriately reflected in spot rates, which are highly reactive to shifting market conditions. As linehaul spot rates remain 51 cents below contract rates, marked signs of rebalancing are beginning to appear, though there is still room for contract rates to decline — or for spot rates to rise — in the first half of 2024.

For more information on FreightWaves Research, please contact Michael Rudolph at mrudolph@freightwaves.com or Tony Mulvey at tmulvey@freightwaves.com.

The post The long road to recovery appeared first on FreightWaves.